Changes to the Annual Investment Allowance (AIA)

The AIA maximum is set to decrease from £1million to £200,000 from 1 January 2021 onwards.

The AIA allows 100% tax relief on qualifying capital expenditure incurred in an accounting period. Any capital expenditure in excess of the AIA maximum would qualify for writing down allowances where tax relief is available at either 18% or 6% per year. The AIA therefore provides almost immediate tax relief on the cost of the capital expenditure, whilst writing down allowances provide for the same amount of tax relief but it is spread over several years.

If your business has a 31 December 2021 year end, the reduction in the AIA will be straightforward with the AIA simply being £200,000 starting from 1 January 2021. If, however, your accounting period straddles the 1 January 2021 there may be some planning required in order to maximise the AIA available to you, particularly if you are anticipating large amounts of capital expenditure. It can be very easy to get caught out by the changes and potentially miss out on significant tax reliefs.

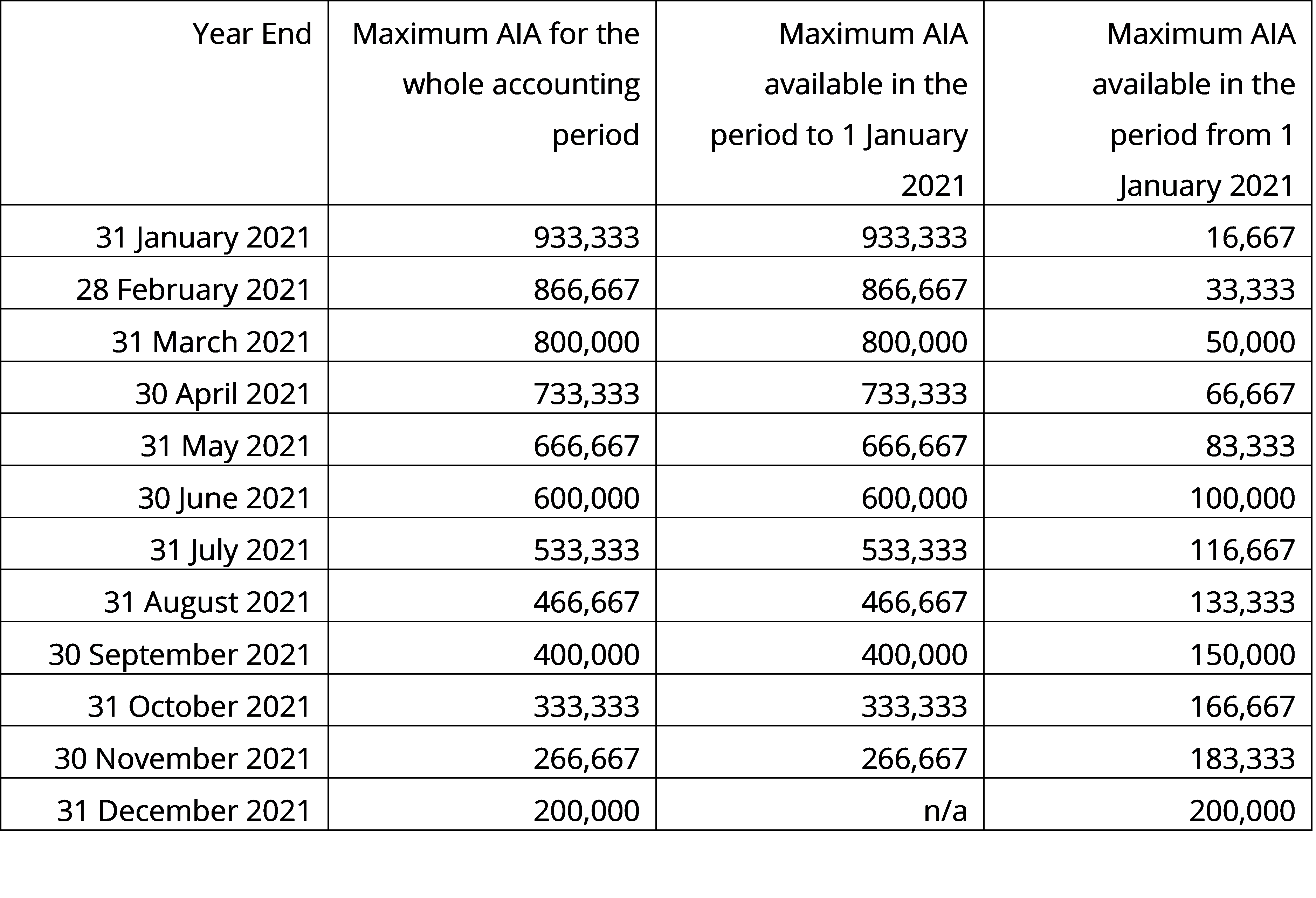

The AIA maximum for an accounting period straddling 1 January 2021 is calculated by reference to the proportion of the year where the AIA maximum was at £1m and the proportion of the year where it was £200,000.For example, for an accounting period ending 31 March 2021, the total AIA available for the year is £800,000, which is made up of 9/12months of £1 million and 3/12 months of £200,000.

There is however a restriction for the amount of AIA available in the period from 1 January 2021.It is restricted to the proportion of AIA that relates to the period from 1 January 2021 to the end of the accounting period. Therefore, for an accounting period ended 31 March 2021, the AIA maximum for the period to 1 January 2021 to 31 March 2021 is £50,000.The period to 1 January 2021 is however only subject to the total AIA maximum for the entire accounting period.

To illustrate this, let’s assume a business incurred qualifying capital expenditure of £1m in its accounting period ended 31 March 2021.£500,000 of the expenditure was incurred in the 9 months to 1 January 2021 and the remainder was incurred in the 3 months after the 1 January 2021.The total amount of AIA available to this business is £550,000 because the maximum AIA in the period from 1 January 2021 is capped at £50,000.If the business had incurred all of its £1m expenditure in the period to 1 January 2021, the total amount of AIA available to the business would have been £800,000.

Businesses may therefore like to consider incurring any planned qualifying capital expenditure before 1 January 2021 to potentially maximise the allowances available.

For accounting periods ending 31 December 2021 and onwards, the available AIA will be £200,000 for a 12 month period, subject to any future increases or decreases that the government may introduce.

If you have any queries regarding the available AIA for your accounting period, or would like any advice about the tax relief, then please do contact us.

Rosie Bennett FCCA

Manager

Rosie joined Evolution ABS in 2012 and became ACCA qualified in July 2017 and has been a client manager for 5 years.

When Rosie isn’t working, she is very active within Young Farmers. Following her role as the the National Federation of Young Farmers chairman in 2023-24 she sits on the board of management for Rural Youth Europe, this involves bringing rural people across Europe together and she is particularily interested in assisting with the high-level running of the organisation.

She also enjoys showing Holstein Dairy Cattle, helping her parents on their dairy and poultry farm and cycling.